The State of Florida sent a letter to Lee County stating municipalities do not have the authority to allow homeowners a percentage (20% in the case of Fort Myers Beach) over the LEEPA structure evaluation for their rebuild.

The state says only the property appraiser has that authority. Everyone, including Lee County property appraiser Matt Caldwell, was caught off guard by the state letter which arrived this morning minutes before the County Board was to consider what percentage they would vote on. Caldwell told Beach Talk Radio his office is working on a plan now. What this means for Fort Myers Beach residents is unknown at the moment.

Here’s the letter the state sent to Lee County Tuesday morning

MARKET VALUE ADJUSTMENT FACTOR

FDEM Office of Floodplain Management, November 8, 2022

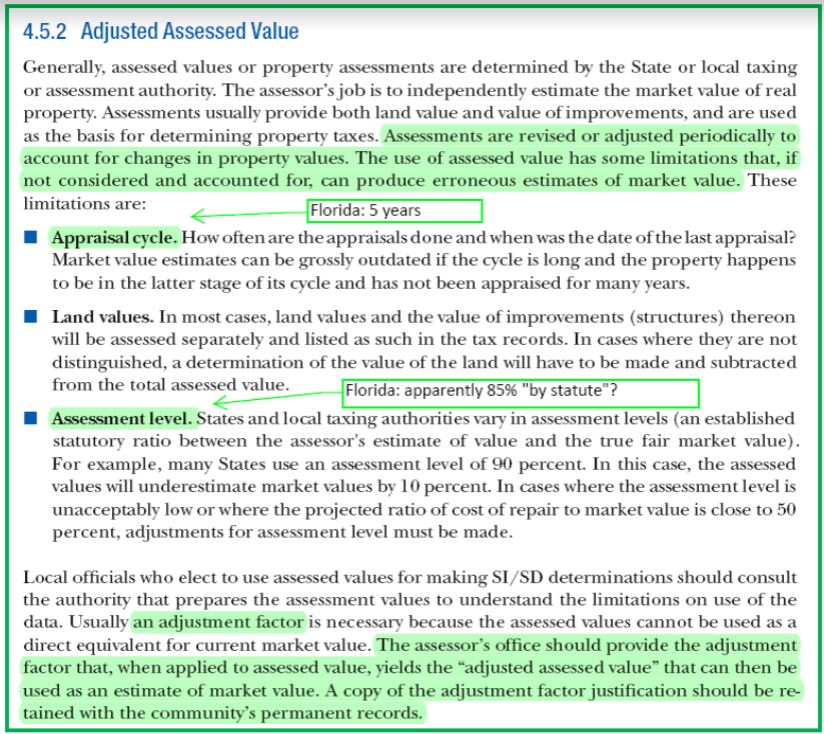

This responds to several questions regarding the use of the tax assessed values of buildings that are determined and published by County Property Appraisers when those assessed values are adjusted by a factor to approximate market value for use in determining whether improvements proposed for buildings in Special Flood Hazard Areas constitute “substantial improvement” (as that term is defined) and whether buildings damaged by any cause have incurred “substantial damage” (as that term is defined). The terms are defined in the Florida Building Code (Building and Existing Building volumes). The terms also are defined in locally adopted floodplain management regulations. For this purpose, the tax assessed value is only the value of the building (excluding land, land improvements, and accessory features such as pools, walkways, fences, and accessory structures).

County property appraisers are charged with deriving a “just valuation” of real property, taking into consideration various factors articulated in Florida Statute, Chapter 193.

We conclude the following:

- Codifying a fixed adjustment factor in the locally adopted definition of “market value” is inconsistent with published FEMA guidance. [See Note 1]

- Codifying a fixed adjustment factor in the locally adopted definition of “market value” is not consistent with the market value definition approved by FEMA Headquarters and FEMA Region IV in 2013. [See Note 2]

- The County Property Appraiser is the appropriate government official to determine adjustment factors, which should be determined within the bounds of the property appraiser’s authority and professional experience.

Therefore, we conclude that local officials who are responsible for making substantial improvement and substantial damage determinations may adjust the published tax assessment value of buildings to approximate market value only when the adjustment factor:

- Is provided, in writing, by the County Property Appraiser,

- Is a single factor, and

- Is provided for a single use for specified individual buildings or, if intended for use for multiple buildings, the Count Property Appraiser specifies the period during which the factor is valid (e.g., 3 months).

Note 1. See FEMA P-758, Substantial Improvement/Substantial Damage Desk Reference, Sec. 4.5.2, “The assessor’s office should provide the adjustment factor…limitation [on use of assessed value] …how often are the appraisals done and when was the date of the last appraisal? Market value estimates can be grossly outdated if the cycle is long, and the property happens to be in the later stage of its cycle and has not been appraised for many years. … [variations] in assessment levels (an established statutory ratio between the assessor’s estimate of value and the true fair market value) … The assessor’s office should provide the adjustment factor… copy of the adjustment factor justification should be retained with the community’s permanent records.” (emphases added).

Note 2. See Florida Model Ordinance, definition “Market Value… or tax assessment value adjusted to approximate market value by a factor provided by the Property Appraiser.” (emphasis added)